Delegated Regulation (EU) 2015/35 supplementing Directive 2009/138/EC of the European Parliament and of the Council on the taking-up and pursuit of the business of Insurance and Reinsurance (Solvency II)

Article 164

Geldend

1.

The market risk module shall consist of all of the following sub-modules:

- (a)

the interest rate risk sub-module referred to in point (a) of subparagraph 2 of Article 105(5) of Directive 2009/138/EC;

- (b)

the equity risk sub-module referred to in point (b) of subparagraph 2 of Article 105(5) of Directive 2009/138/EC;

- (c)

the property risk sub-module referred to in point (c) of subparagraph 2 of Article 105(5) of Directive 2009/138/EC;

- (d)

the spread risk sub-module referred to in point (d) of subparagraph 2 of Article 105(5) of Directive 2009/138/EC;

- (e)

the currency risk sub-module referred to in point (e) of subparagraph 2 of Article 105(5) of Directive 2009/138/EC;

- (f)

the market risk concentrations sub-module referred to in point (f) of subparagraph 2 of Article 105(5) of Directive 2009/138/EC.

2.

The capital requirement for market risk referred to in Article 105(5) of Directive 2009/138/EC shall be equal to the following:

where:

- (a)

the sum covers all possible combinations i,j of sub-modules of the market risk module;

- (b)

Corr(i,j) denotes the correlation parameter for market risk for sub-modules i and j;

- (c)

SCRi and SCRj denote the capital requirements for sub-modules i and j respectively.

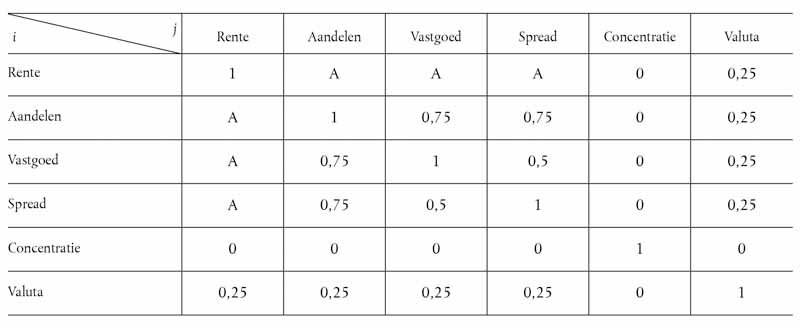

3.

The correlation parameter Corr(i,j) referred to in paragraph 2 shall be equal to the item set out in row i and in column j of the following correlation matrix:

The parameter A shall be equal to 0 where the capital requirement for interest rate risk set out in Article 165 is the capital requirement referred to in point (a) of that Article. In all other cases, the parameter A shall be equal to 0,5.